Cyber insurance has become a vital safety net for organizations of all sizes. It covers financial losses from data breaches, ransomware attacks, business email compromise, and other cyber incidents, including costs for recovery, legal fees, notification, and business interruption. As cyber threats grow more sophisticated and frequent, businesses increasingly rely on these policies to avoid devastating financial hits—average breach costs hover around several million dollars, and without coverage, many small or mid-sized firms could face closure.

In 2026, the cyber insurance landscape is in flux. Premiums have softened after years of sharp increases, but new risks from artificial intelligence (AI) and supply chain vulnerabilities are reshaping policies and underwriting. Staying informed helps companies secure the right coverage and build stronger defenses.

Why Cyber Insurance Matters More Than Ever

Digital transformation has expanded attack surfaces—cloud services, remote work, and connected devices create more entry points for criminals. A single successful attack can lead to data loss, downtime, regulatory fines, and reputational damage. Cyber insurance steps in where traditional policies fall short, paying for crisis response teams, forensic investigations, and even some ransom-related expenses (depending on the policy). Without it, organizations bear the full brunt, which explains why demand continues to surge even as the market evolves.

Key Causes and Ongoing Issues

The core drivers behind the need for cyber insurance stem from escalating cyber threats. Ransomware remains dominant, often involving double or triple extortion (data theft, encryption, and public shaming). Business email compromise and funds transfer fraud account for many claims, while supply chain attacks ripple across industries when vendors get hit.

Insurers face their own challenges. Large losses in recent years prompted tighter terms: exclusions for “acts of war” or state-sponsored attacks, limits on paying ransoms, and new clauses denying coverage for known vulnerabilities (CVE exclusions). Claims can be rejected if companies fail to meet basic security requirements like multi-factor authentication (MFA) or regular patching. This creates a coverage gap—businesses think they’re protected, only to discover exclusions or unmet conditions during a claim.

Rising severity adds pressure. While claim frequency dropped for some carriers in 2025, the cost per incident climbed, especially in ransomware cases. AI tools let attackers scale operations faster, using deepfakes for social engineering or automating phishing at unprecedented levels.

Latest Developments and Market Reports

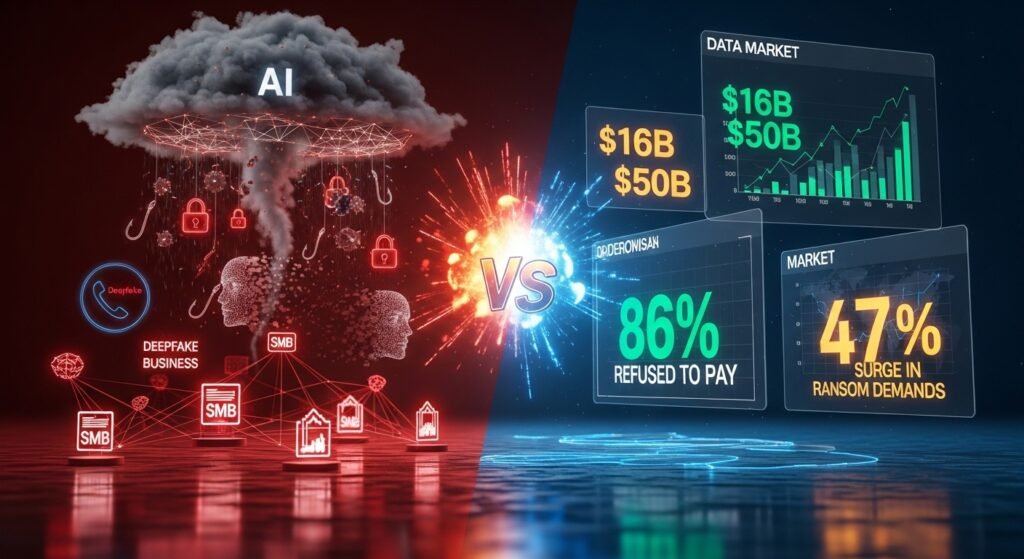

The cyber insurance market entered 2026 in a buyer-friendly phase after significant softening in 2025. Premiums fell by an average of 11% globally, with further reductions expected in the first half of 2026, and many policies now offer broader coverage. Global premiums reached roughly $16 billion in 2025 and are projected to climb toward $30–50 billion by 2030, driven by growing awareness and new risks.

Recent claims data shows mixed trends. Coalition’s 2026 Cyber Claims Report revealed initial ransom demands surged 47% year-over-year in 2025, yet a record 86% of businesses refused to pay thanks to better backups and incident plans. Ransomware still drove the highest average losses ($269,000 per claim), but business email compromise and funds transfer fraud made up the bulk of notifications.

AI is emerging as a game-changer. Insurers now scrutinize AI-related exposures, from biased algorithms causing liability claims to deepfake-enabled fraud. Quantum computing threats loom on the horizon, potentially breaking current encryption, though most experts say practical risks remain years away. Regulatory pressures—new state AI transparency rules and privacy laws—also influence coverage wording.

YouTube discussions provide timely, expert perspectives that add depth to these reports. In Gallagher’s “Cyber Insurance Market Outlook 2026” video, Managing Director John Farley and Cyber Practice Leader Dan Burke describe 2026 as a pivotal year for AI risk management. They note ransomware evolving into targeted multi-extortion attacks and highlight deepfake technology making social engineering far harder to detect. The experts stress contingent business interruption coverage for supply chain risks and urge companies to review data governance and vendor security scoring. They predict cyber insurers will lead on AI-specific wording as regulations proliferate across U.S. states.

Another insightful video, “Cyber Insurance in 2026: Why Prices Are Flat but Risks Are Rising,” explains that stable or slightly declining premiums result from widespread adoption of basic “cyber hygiene” practices like MFA, encryption, and backups. However, attacks on small and medium businesses are surging, with AI driving a sharp rise in ransomware and shadow IT (personal devices used for work) accounting for many breaches. The host recommends shopping renewals now while competition remains high and emphasizes employee training to counter deepfakes and wire fraud.

Overall, 2026 marks a turning point: the market favors buyers for now, but signs of tightening appear as loss severity grows and insurers demand stronger controls.

Practical Solutions, Tips, and Troubleshooting

The good news? Businesses can improve their position through proactive steps. Strong security practices often lead to lower premiums, higher limits, and fewer exclusions.

Key Tips for Better Coverage:

- Implement core controls: Enable MFA everywhere, maintain encrypted backups tested regularly, patch systems promptly, and use endpoint detection tools. Insurers reward these with better terms.

- Review policies carefully: Look for clear ransomware coverage, no overly broad war exclusions, and explicit AI-related language. Compare multiple carriers—wording varies widely.

- Assess third-party risks: Score vendors on cybersecurity and build contingency plans for supply chain outages.

- Build an incident response plan: Include legal, PR, and forensic partners upfront. Test it annually.

- Train staff: Focus on recognizing phishing, deepfakes, and verification protocols for money transfers.

Troubleshooting Common Problems: If a claim is denied, first verify you met all pre-incident controls (e.g., MFA was active on the affected systems). Gather evidence of compliance and appeal—many denials stem from documentation gaps rather than total exclusions. Work with a broker experienced in cyber claims to negotiate. For ransom situations, note that many policies now encourage refusal through strong backups, but confirm your specific wording.

Small businesses should start with affordable standalone policies or endorsements on existing packages. Larger firms may need tailored limits for systemic risks. Shopping around in the current soft market can yield 5–15% savings for well-prepared organizations.

Conclusion and Final Advice

Cyber insurance news in 2026 paints a picture of opportunity mixed with caution. Premiums are more affordable and coverage broader than in recent hard-market years, but AI-driven threats, sophisticated extortion, and regulatory shifts demand vigilance. The market’s growth to tens of billions by 2030 shows insurers are adapting, yet success depends on organizations matching that progress with robust security.

The smartest move? Treat cyber insurance as one layer of a broader resilience strategy. Combine strong technical controls, employee training, and regular policy reviews with ongoing threat monitoring. Consult a specialized broker, watch expert discussions on platforms like YouTube for real-time insights, and stay proactive. In a world where one click can cost millions, preparation today ensures survival and recovery tomorrow. Businesses that act now will be best positioned as the cyber insurance landscape continues to evolve.

FAQs

Cyber insurance protects organizations from financial losses caused by cyber incidents such as ransomware attacks, data breaches, and business email compromise. In 2026, rising AI-driven threats and increasing breach costs make this coverage a critical part of business risk management.

Most cyber insurance policies cover expenses related to incident response, data recovery, legal fees, regulatory fines, customer notification, and business interruption. Some policies may also cover ransomware payments depending on the terms and security compliance.

Premiums softened in 2025 and early 2026 due to improved cybersecurity practices like multi-factor authentication, backups, and stronger security controls. Increased competition among insurers has also created a more buyer-friendly market.

Artificial intelligence is transforming both cyber threats and risk assessment. Insurers are beginning to evaluate AI-related liabilities such as deepfake fraud, automated phishing attacks, and algorithmic risks when underwriting cyber policies.